Scared Strait: Ending Iran’s Threats to Hormuz and the Gulf

Click here to download the JINSA Insight.

Executive Summary

Without actually closing the Strait of Hormuz or denying the sea to the U.S. Navy, Iran has brought Gulf shipping nearly to a halt and upended the global economy. Despite President Trump’s blandishments, shippers will refuse to transit these waters as long as the perceived risks remain prohibitive and Iran’s maritime threats appear plausible—even if they no longer are formidable.

These threats are mainly in the Gulf, not the Strait. As its other anti-ship capabilities are degraded, Iran will have greater incentive to prolong the war and raise its costs by dotting the Gulf—currently devoid of U.S. surface ships—with naval mines. Just as shipping is easier to stop than to restart in wartime, mines work in Iran’s favor by being relatively easy to deploy, difficult to clear, and potentially paralyzing to seaborne traffic.

Before commercial shipping can be escorted, the first order of business is to forcefully and proactively reassert U.S. military dominance in the Gulf. Sailing through Hormuz at will, demonstrating our ability to hold the sea, preventing Iranian minelaying, and projecting air and naval power in Gulf itself are necessary to create the permissive environment for escorting commercial vessels and restoring freedom of navigation. Ultimately, this will be less costly and time-consuming than remaining outside the strait until Iran’s maritime military capabilities are utterly eroded. Failing to do so, and letting Tehran think it holds the keys to lock up the Gulf, poses far more enduring challenges than the current shutdown.

Ships in a Bottle

Without actually closing the Strait of Hormuz, Iran’s threat to this vital shipping lane and surrounding waters is triggering the largest energy disruption in history. Like its attacks on Gulf critical infrastructure and other assets ashore, this reflects the regime’s goal to win to the war by making its economic and political costs unbearable for the United States.

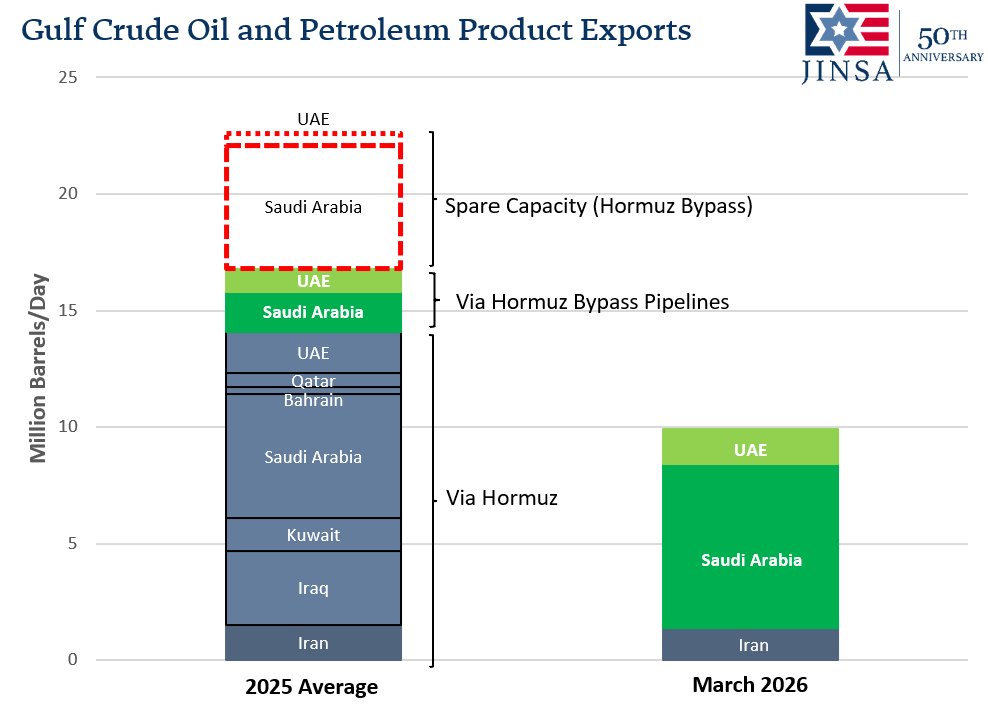

Prewar, one-fifth of global petroleum liquids and liquefied natural gas (LNG) consumption transited the strait, making it perhaps the world’s most-important energy chokepoint. Even larger percentages of global fertilizer and industrial helium supplies, anywhere from one-third to one-half, also pass through the strait. Current hostilities, including Iranian attacks on tankers and other commercial vessels, have shrunk Hormuz shipping by fully 90 percent and bottled up 600 international trading ships inside the Gulf. A majority of that remaining 10 percent is Iranian oil exports, some 1.0-1.5 million barrels per day (bbl/d), as well as ships from China and other friendly countries that Tehran deigns to “permit” safe transit.

Alternative outlets like Saudi Arabia’s East-West Pipeline to the Red Sea and the Emirati (UAE) Habshan-Fujairah Pipeline to the Gulf of Oman can redirect no more than one-third of these disrupted oil supplies, and none of the LNG (see chart and map). Moreover, Iran has struck export facilities and tankers near Fujairah repeatedly, and Tehran’s Houthi proxy in Yemen has shown real capability to disrupt shipping along the Red Sea—including the East-West Pipeline’s terminal at Yanbu and other Saudi energy hubs. With their storage tanks full and no ships taking on new supplies, Arab Gulf countries have scaled back oil production by at least 10 million bbl/d, and the world’s second-largest LNG exporter, Qatar, has halted such output altogether. The global oil market’s normal ability to absorb much of this shock is negated by the fact that most crude oil spare production capacity is now stranded in Saudi Arabia and the UAE.

Iran’s ability to throttle back shipping is disproportional to its kinetic action and its remaining capabilities. Its naval forces, now largely destroyed or in the process of degradation, cannot deny the sea to the U.S. Navy in a direct confrontation. But even with its dwindling arsenals, Iran’s projectile strikes on some 16-20 commercial vessels in the Gulf and Hormuz, and its jamming of their communications and navigation, have convinced shippers that the risk of losing their vessels and crews is prohibitive.

Importantly, these perceived dangers are at least as much physical as financial. Insurance coverage remains available but, even with President Trump’s proposal to cushion rising rates through U.S. government-backed reinsurance, these policies are finding few takers. When pressed by the president why Iran could so successfully choke off shipping, Chairman of the Joint Chiefs Gen. Dan Caine noted how “even one Iranian soldier or militia member zipping across the narrow neck of the strait in a speedboat could fire a mobile missile right into a slow-moving supertanker, or plant a limpet mine on its hull.”

Such perceptions are not easily assuaged. Even six months after the Houthis stopped attacks around Bab el Mandeb, and despite the costs of rerouting around the Cape of Good Hope, seaborne traffic still has not normalized in this crucial chokepoint. Similarly, the belief that Iran’s de facto blockade will persist is as consequential for the global economy as perceptions of current risk. Iran’s one-off strike on Saudi oil facilities in 2019 triggered a temporary if sizable spike in oil prices from which the global market, and Riyadh’s output, recovered fairly quickly. But now, with no relief in sight, energy prices hikes could prove more durable as traders assume that, going forward, global prewar consumption must fall in tandem with the loss of vital Middle East exports. Tellingly, President Trump’s March 9 statement, that the war would end soon, offset this larger trend only temporarily.

The Gulf, Not Hormuz, is the Chokepoint

Iran’s asymmetric achievements are focusing attention on the most glaring geographic chokepoint: the narrow Strait of Hormuz, which funnels so much shipping through a 30-mile-wide outlet with two, mile-wide navigable channels in the center. Reporting frequently lumps together this logical pressure point with another—the threat of naval mines, which can wreak ample havoc on shipping. But Iran’s incentives and ability to mine Hormuz are low compared to the Gulf, which offers much greater returns on even limited investments.

Iran reportedly has deployed roughly a dozen mines in or near the strait, but likely this reflects its intent to deter commercial shipping rather than actually try to seal off the waterway. Generally the channel is too deep for bottom or moored mines, and its currents too swift for drifting mines, to work reliably. Mining this chokepoint with any precision, and coordinating these operations with other Iranian forces, is further complicated by Tehran’s prewar decision to disaggregate its military command and control (C2), and subsequently by extensive U.S.-Israeli targeting of these C2 nodes. These factors also directly undermine Iran’s ability to guarantee safe transit for its ships and those of countries it deems friendly.

Mining inside the Gulf is more attractive. Its generally shallow waters force Very Large Crude Carriers (VLCC) and LNG carriers to traverse lengthy, narrow, and predictable paths that can accommodate their drafts. These paths can be endangered by Iran’s panoply of naval mines, without the drawbacks of Hormuz. Iran can be more profligate and imprecise when sowing large fields of drifting mines out in the Gulf, since they are less likely to threaten its own coastline or ships. This serves Iran’s wartime goals by complicating mine clearance efforts and amplifying shippers’ fears. Bottom and moored mines likewise become more credible threats in the Gulf’s shallower waters. Notably, Iran’s and Iraq’s extensive naval mining in the 1980s did not center around Hormuz, but instead on these main shipping arteries in the Gulf, where at least four major minefields were laid (see second map).

Mining the Gulf also becomes more likely as Iran’s other anti-ship capabilities erode. The Revolutionary Guard’s (IRGC) capacity to threaten shipping with missiles, coastal defense batteries, fast attack boats, and radars is increasingly the target of U.S. operations. Though also subject to U.S. attack, the IRGC’s drone, small boat, and mine arsenals are likely its most resilient and impactful remaining capabilities on this front. These are relatively simple to manufacture, plentiful—perhaps some 5,000, in the case of mines—and easy to disperse and deploy. This includes hit-and-run operations from Iran’s rocky secluded coastline, and minelaying by “little green men” ostensibly engaged in civilian maritime activities. And unlike its anti-ship missiles, Iran’s drones are proven to inflict real damage on commercial vessels. Its anti-ship drone arsenals likely include unmanned surface vessels (USV), similar to those employed successfully by the Houthis and Ukraine.

Mining is Easy, Demining and Escorting Are Hard

Just as shipping is much easier to stop than to restart, mines are far more difficult and time-consuming to remove than to emplace. From Tehran’s perspective, mining offers the added benefit of dragging out and compounding the economic paralysis of this conflict, since the perceived threat of even small numbers of mines can bring seaborne traffic to a halt until they are found and neutralized—a task made even more challenging in wartime.

In both world wars, German mining of British ports, estuaries, and the North Sea inflicted serious losses on Allied naval and merchant ships, and forced the Royal Navy to divert precious resources to minesweeping. For all the devastating strategic bombing of its core urban areas, Japan was only threatened with starvation and industrial extinction once U.S. forces started mining its shores and internal waters in mid-1945. Minimal American minelaying shuttered North Vietnam’s main port of Haiphong in 1972, while North Korean and Iraqi sea mines delayed and dissuaded U.S. amphibious invasions in 1950 and 1991, respectively. In the latter case, U.S.-led postwar demining efforts took nearly two months, even with the benefit of maps provided by Iraq. Covert Libyan minelaying in the Red Sea in 1984 impacted Suez Canal traffic for even longer before the seas could be cleared.

Whether to protect against mines or other threats, naval escort operations likewise are time-consuming and complex. The transatlantic convoy system of World War II and escort operations during the Iran-Iraq War, which included reflagging Gulf Arab tankers, required months to coordinate intricate U.S.-led planning and assemble needed military assets—including from partner countries—before they could transit contested waters. In the latter case, these broader U.S. efforts included setting up Gulf bases ashore and afloat to preempt naval mining and counter Iran’s other threats to tanker escorts.

Recommendations: Retaking the Gulf

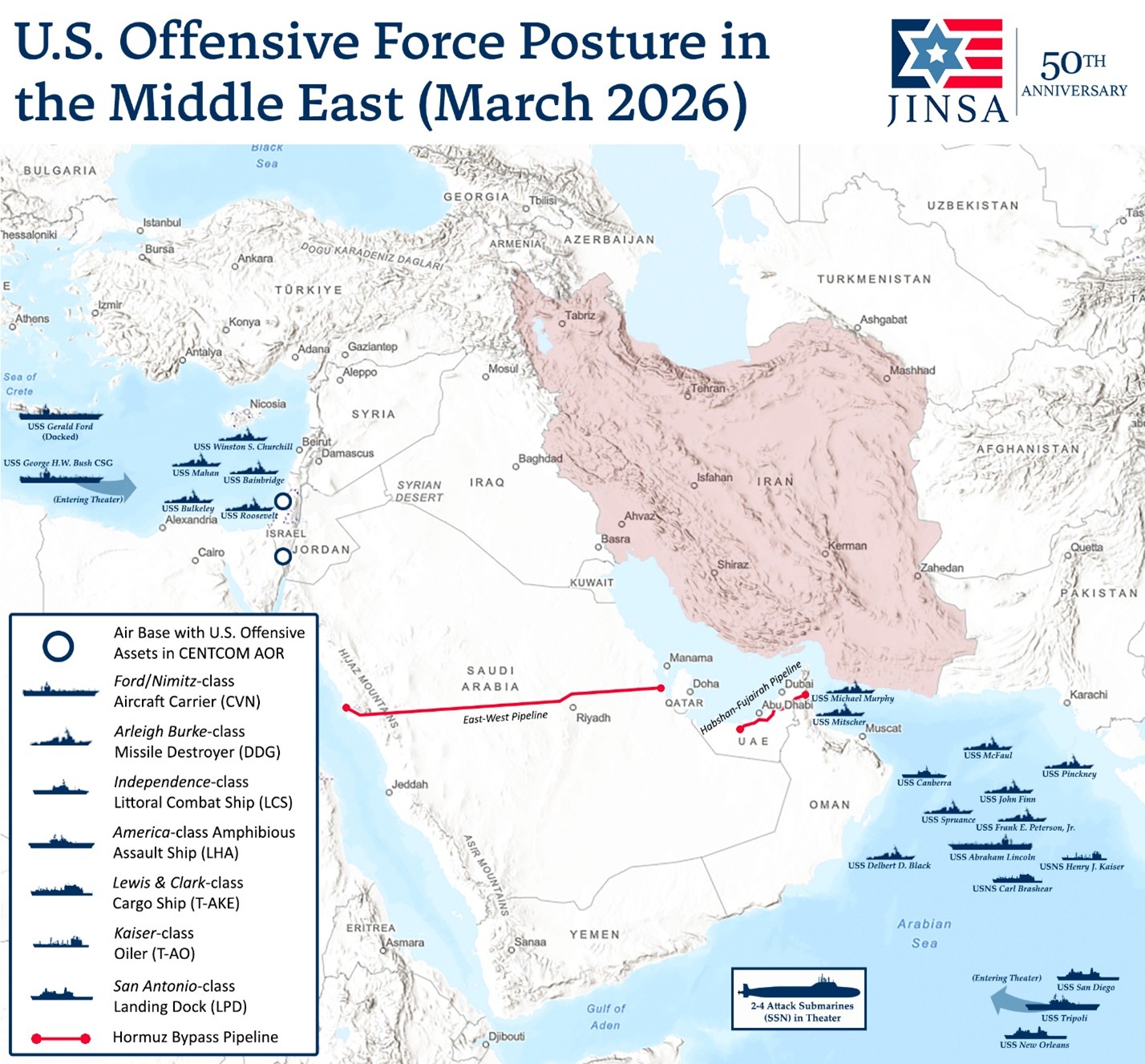

To date, there are no reported U.S. surface ships operating in Hormuz or the Gulf, effectively ceding these areas to Iran (see first map). Despite President Trump inveighing commercial ships to resume transits on their own, the perceived risks of doing so will remain prohibitive until friendly warships and/or U.S.-flagged vessels show they can sail through these waters unimpeded. With the same urgency that it is targeting Iran’s maritime threats, the United States, with its allies and partners, should prioritize reasserting naval predominance in one of the world’s most important waterways.

Doing so as swiftly and forcefully as possible is necessary for several reasons. Iran’s motivation to mine the Gulf, and prolong the conflict at relatively little cost to itself, will only grow as its other military assets are progressively degraded, and doing so will be easier if it rules the Gulf’s waves. Even once these threats are neutralized or severely eroded, prior Gulf and Red Sea disruptions suggest shipping and energy production could take weeks or months to resume normal operations—all the more so with the Gulf’s massive backlog of tankers and other ships.

Perhaps most crucially, the way this war ends will determine the future of free navigation in the Gulf and Hormuz. Assuming the regime does not collapse, it likely will retain and reconstitute at least basic drone, small boat, and naval mine arsenals, and perhaps anti-ship missiles as well. To the extent Tehran believes it successfully locked up Hormuz and the Gulf, defied the U.S. military, and split America from partners that depend heavily on Middle East exports, it will continue acting as if it holds the keys to the global economy—giving it a degree of deterrence and predominance it did not possess prewar. Invalidating Tehran’s theory of victory, therefore, will have ramifications for this war and potentially the next. In this light, striking Iranian energy infrastructure, even if logical for other reasons, will not affect the regime’s underlying inducements to threaten the Gulf and Hormuz.

Ending Iran’s threats to shipping and the global economy, and signaling U.S intent to restore freedom of navigation, first requires U.S. forces to move into the Gulf and prevent Iranian mining before commercial vessels can be escorted or otherwise move into open seas. Overall, this entails two complementary, parallel, and urgent lines of effort:

- Getting serious about protecting Hormuz and the Gulf, reasserting naval predominance over Iran, and creating a permissive environment for escort operations by:

- Sailing U.S. Navy warships through Hormuz and reestablishing presence in the Gulf.

- Conducting maritime overwatch and anti-surface warfare missions in the Gulf with U.S. Air Force close air support (CAS) aircraft, U.S. Army light helicopters, and potentially other surveillance and attack platforms to prevent Iranian minelaying.

- Leveraging Saudi, Emirati, and other Gulf countries’ clear desires to degrade Iran’s military threats by convincing them to provide naval capabilities and basing access.

- Using these capabilities as a zone defense, providing an outer layer of protection for the point defenses of warships, mine countermeasures (MCM) ships, USVs, airborne MCM helicopters, and other escort platforms against residual Iranian maritime threats.

- Coordinating with European NATO partners and others to enforce UN Security Council, U.S., and EU sanctions by forcibly interdicting Iran’s revenue-generating “shadow fleet.”

- This “Venezuela” quarantine option is less risky, and likely at least as effective, as seizing Iran’s primary energy export hub deep inside the Gulf at Kharg Island.

- Implementing existing plans under U.S. Central Command (CENTCOM), and amassing coalitional forces, to escort commercial vessels by:

- Redeploying MCM littoral combat ships (LCS) from the Indo-Pacific to the Middle East.

- Working with European, Asian, and Gulf partners to provide additional MCM ships, escort warships, and other platforms.

- Earlier this week the European Union’s foreign policy chief said various options are in play to potentially lend support, and certain European NATO forces have recent relevant experience escorting merchant vessels in the Red Sea and supporting maritime security in the Gulf.

- Exercises under CENTCOM’s auspices have rehearsed multilateral maritime security operations regularly in recent years.